Workshop on Common Inspection Findings by AOB

Bukit Kiara, KL: On Monday, May 27, a pivotal workshop was held addressing the main issues related to the Audit Oversight Board (AOB) inspection processes, organized by the Malaysian Institute of Certified Public Accountants (MICPA) in collaboration with Securities Commission Malaysia (SC). The workshop was attended by representatives from JAP, including our Partner (Ms. Fatimah) and Directors (Mr. Hanif Amin & Mr. Firdaus Nasir), alongside other audit and accounting firms representative. This gathering was not only a platform to discuss common inspection findings by the AOB but also to suggest effective remediation measures and what AOB auditors should do. The event underscored the importance of continuous improvement and adherence to high standards in audit quality, in line with the MICPA’s ongoing efforts.

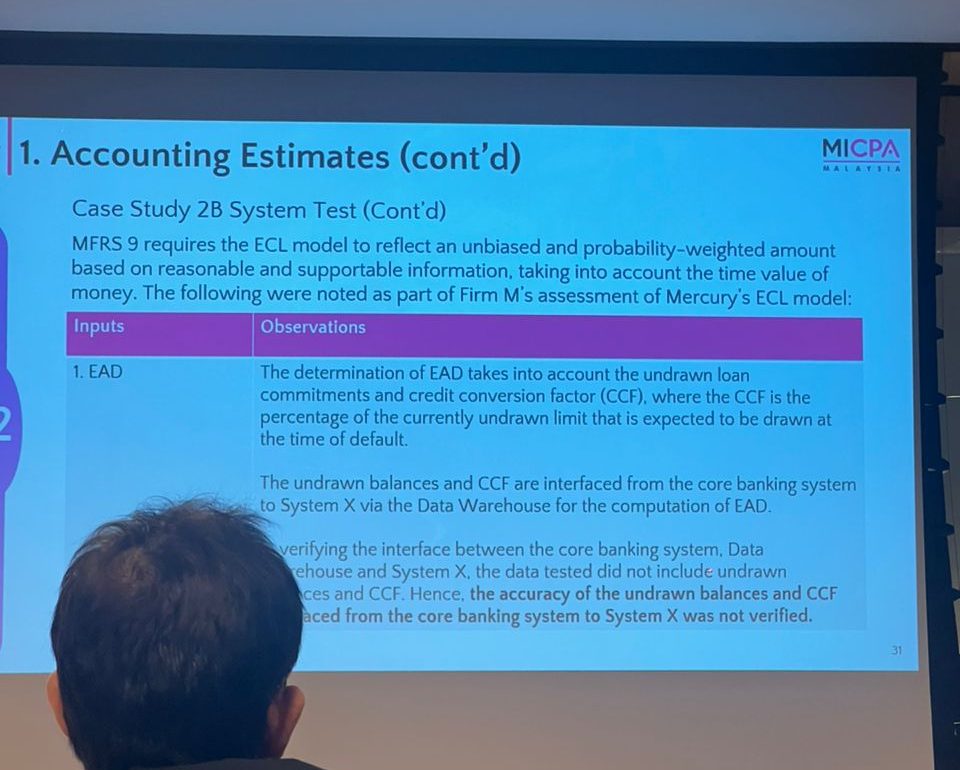

During the workshop, key findings from recent AOB inspections were discussed. Some of the most prevalent issues identified included:

- Inadequate Documentation: Auditors often fail to maintain comprehensive documentation to support their audit findings and conclusions.

- Insufficient Audit Evidence: There are instances where auditors do not gather enough appropriate audit evidence to substantiate their opinions.

- Weak Internal Controls Testing: Audits frequently reveal insufficient testing and evaluation of a company’s internal controls.

- Risk Assessment Deficiencies: Auditors sometimes exhibit inadequate assessment and response to risks of material misstatement.

- Non-Compliance with Auditing Standards: A noticeable number of audits show non-compliance with established auditing standards and guidelines.

It was a critical step towards addressing the inspection issues identified by the AOB. By sharing insights and remediation strategies, and promoting continuous improvement, the event reinforced the commitment of JAP and other participants to uphold the highest standards in audit quality. MICPA’s efforts in fostering an environment of excellence and continuous learning will undoubtedly contribute to the integrity and reliability of financial reporting in Malaysia.